BUSINESS FIRE INSURANCE 101

Fire Insurance is no stranger when it comes to business assurance. Besides Burglary Insurance, Fire insurance is one of the compulsory insurances physical Malaysian business owners require. Second to Motor Insurance, Fire Insurance is the biggest general insurance policy in the market — with over 40% market share in total gross premium for the year 2016.

But as a business owner yourself, what does Fire Insurance mean for you?

Say you built a career as a property investor, and you own a couple of factory outlets that are free of bank loans. By continuing to pay your annual property taxes to the local council, you have every right to do as you please with your property. Be it leaving them un-tenanted or even renting them out within the boundaries of the law.

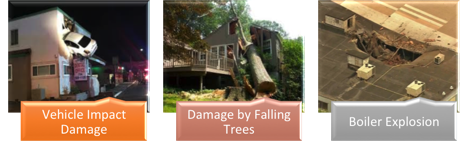

However, in the event that 1) a massive thunderstorm hits the area, 2) a giant tree falls onto one of your factory outlets, and 3) severe damages have been inflicted on to the infrastructure of your building, whom do you think is responsible to cover the cost of repair for the damages?

If you’re not sure, don’t worry. A survey was recently conducted by the PIAM (Persatuan Insuran AM Malaysia) where the same scenario was presented to a group of business owners who own a Fire Insurance policy. The findings are that:

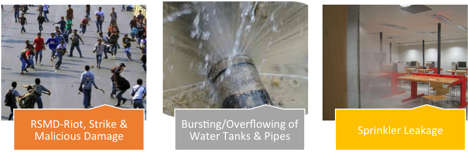

- Majority of these policyholders believe that their Fire Insurance policy will cover them in the event that a giant tree falls and inflicts damages on their premise

- 1/3 of these Fire Insurance policyholders also believe that flood damage will be covered by their basic Fire Insurance policy

Although it is not wrong to assume as such, it is important for these clients to note that these are considered as additional coverages under the Fire Insurance policy. And with additional covers, comes additional premiums that can be made and agreed upon with the insurance company.

Already Know What you Want?

WHAT IS FIRE INSURANCE?

First thing you need to know about Fire Insurance is that there is no specific fire damage insurance that one can purchase in the insurance guidebook. However, there are several types of coverages that can be insured in the event that there is fire to the building.

For example, business owners can insure their buildings’ value with Buildings Insurance to cover the cost of re-building, whereas Contents Insurance can cover the cost of repairing or replacing damaged furniture and/or appliances in the event of a fire. If the nature of your business is based on trades, where stocks would need to be kept in the factory, this too, can be added as an additional coverage to your Fire Insurance policy.

Whilst Buildings Insurance can cover the cost of re-building a property in the event of total damage or destruction due to a fire, Contents Insurance on the other hand, can cover the cost of repairing or replacing damaged furniture and appliances in the event of a fire.

Additional items covered by Fire Insurance at a cost is as per below:

WHO IS FIRE INSURANCE FOR?

Just like vehicle ownership, any business owners who have a business loan for their property with any banks are required to insure their property with Fire Insurance.

But since majority of businesses have property loans, the worry isn’t with having their basic insurance covered. When it comes to time of claims, many policyholders find inadequacy in their coverage and file for dispute during the claim processes. It is vital for policyholders to check and agree on their policies prior to disastrous events.

However, if you are renting your business premises, you don’t need to take up fire insurance on the building. Instead, you would need to take the Fire Insurance on the basis of improvements, furnishings and fittings on your policy to cover the changes you made to the property

Already Know What you Want?

HOW TO DETERMINE FIRE INSURANCE RATE

To determine the Fire Insurance rate for a business owner, here are several key factors that are taken into considerion:

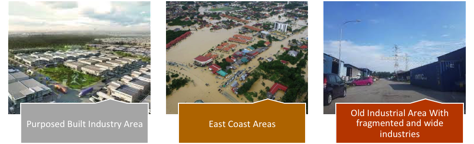

- Location of Risk

A Fire Insurance policy tends to be cheaper when the property is located in the city area compared to rural or east coast areas, which are prone to flood claims every year.

If the building is in an industrial area, the basic premium would tend to be cheaper due to wide amenities of firefighting appliances such as fire extinguisher, water fire extinguisher and the overall planning would minimize the risk of fire spreading to adjacent unit’s unless it is started in the factory itself.

- Sum Insured

A major component in the price of Fire Insurance is the Sum Insured of your assets. For example, if a building reinstatement value is above RM10 million, then it falls under the Fire Insurance self-rating that is determined by the insurer with the guideline provided by PIAM. With the recent de-tariffication ruling, certain types of occupations that operate from within the business premises would get more rebates on premiums. Many insurance companies also offer free evaluation reports for properties that are total up to more than RM50 million Sum Insured as a complimentary package.

(c) Age of Building

The age and maintenance structure of a building plays a crucial part in the determination of its fire insurance rates. Majority of buildings, which are over 10 years old, have not had replacement in buildings wires or a forensic audit, as it is not required by the Fire department during renewal of the license.

(d) Other information required

- The flow chart of its manufacturing process for manufacturing risks

- Exposures from adjacent buildings

- Additional Perils Required

Already Know What you Want?

CLAIM PROCEDURE FOR MALAYSIA BUSINESS FIRE INSURANCE

To proceed for a claim to recover the loss from your business, a number of information is needed by the appointed adjuster, such as completed claim form, police report, photographs, invoices and etc.

Many may not know this, but a majority of business owners do tend to misplace supporting documents and are unable to proceed with the claim imbursement. Such examples would include missing invoices and proof of purchases for damaged printer due to bursting, or even overflowing of water tank, pipes and apparatus in the building.

However, you won’t need to worry. With our online system, our insured policyholders are able to upload a photo and/or invoice of the purchased material or goods to our database during application process. This is especially useful in the event of claim processes.

If the claim amount is higher than RM5,000.00, an estimate cost of repair should be submitted to the insured via an official quotation. The adjuster appointed by the insurance company would also request for additional documents that are not listed as above.

For your notice, documents required by adjuster are as per below:

- Claim form by insurance company

- Photographs and Invoices of damaged items

- Official Quote

- Any other supporting documents

Our Malaysian Business Insurance Calculator Solution.

With our invention, we are building a customer-centric online product that is intuitive and responsive. We are re-making the cycle of SME’s getting their business insurance. Our software is based on getting the average premium for business insurance relevant to each industry and small medium enterprises.

SME is widely involved in and propose to the website user. It provides a general view of the industry insurance premium for SME’s. Also our business insurance calculator provides a guideline to open their own negotiation with insurance companies to get an industry rate. Our innovation is simple yet effective in filling the gap between insurance companies and their distribution channel.

With the advent of technology, business owners now expect to deal with insurance online. In the same way they use consumer friendly online technologies to deal with banking, payroll, accounting or sales. Online technologies equals convenience. The way businesses are treated in the current cycle is also very frustrating and outdated.

We have linked with various insurance companies to use their API system for an online seamless insurance issuance. Our systems allows policies to be issued with only a few clicks.